If you received a letter (sample letter) from the Henrico County Department of Public Works informing you that your parcel was removed from the FEMA Special Flood Hazard Area (SFHA) or the amount of FEMA SFHA on your property decreased, this page will help you understand the next steps for protecting you and your property. The updated maps went into effect on April 25, 2024 for flood insurance and regulatory purposes.

Next Steps

I. Understand Your Flood Insurance Options

If your building is identified to be in a moderate- or low-risk area with the effective maps, you are not required by law to purchase flood insurance if you carry a mortgage from a federally regulated or insured lender. However, your lender may still require you to have flood insurance coverage.

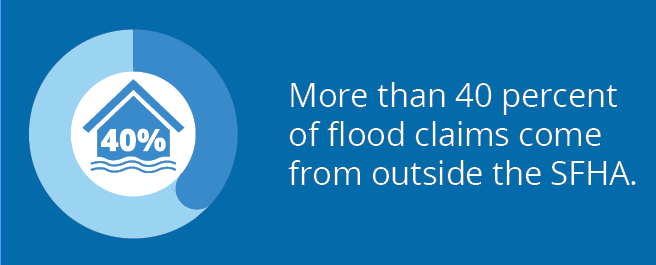

Although your flood risk may be moderate to low, there is still risk to your property. Flood insurance is still strongly recommended in these areas. In fact, National Flood Insurance Program (NFIP) policyholders outside of mapped high-risk flood areas file more than 40% of all NFIP flood insurance claims.

Buildings in these areas may still be subject to regulatory requirements if located in the 500-year floodplain or within 40 feet of the SFHA.

Renting or Leasing?

If you are leasing a home or business, keep in mind that while your landlord may have flood insurance to cover their building, that insurance will not cover your personal belongings. Only a separate flood insurance policy can cover items damaged in a flood. Protect yourself with a flood insurance contents coverage policy. Your insurance agent can help you acquire a policy and answer questions.

III. Take Steps to Protect Your Property

In addition to flood insurance, there are measures you can take to protect your property.

- Install flood vents in the foundation walls of the building to help protect the structure from flood damage by reducing the pressure from flood waters

- Elevate air-conditioning units and furnaces or create a shield to divert water to protect your utilities or appliances from flooding. Efforts such as these will not only protect the equipment in a flood, they may also provide a discount on flood insurance.

- Maintain proper water runoff and drainage. Routinely clean and maintain gutters, downspouts, and splashpads so that rainwater from your roof flows easily away from your home. Also, make sure that any nearby drainage ditches or storm drains are clear of debris and functioning properly.

- Improve lot grading. Determine how water flows or accumulates around your home to identify potential trouble spots (often easy to see during an average rainstorm). Stormwater should always drain away from the building; if necessary, change your landscaping to improve runoff. This may include building up any sunken areas around the foundation, digging small depressions to properly channel water, and otherwise improving the yard so that it slopes away from your home.

III. Understand Requirements for Future Improvements to Your Property

Special permit requirements and development standards must be fulfilled in both the SFHA and its adjacent areas. Before you build, fill, or alter your land or the building(s) on your property, be sure to visit the County’s Floodplain Permits webpage to determine if you need a permit.

Abbreviations

FEMA – Federal Emergency Management Agency

NFIP – National Flood Insurance Program

SFHA – Special Flood Hazard Area

Do I Need Flood Insurance?

Risk levels outside of the SFHA might be reduced, but not removed, so obtaining a policy is recommended. Policyholders outside of mapped high-risk flood areas file more than 40 percent of all NFIP flood insurance claims.