Imputed benefits are non-cash benefits provided by an employer to an employee that have a monetary value and are considered taxable income by tax authorities, even though the employee doesn’t receive actual cash.

Definition

Imputed benefits (also called fringe benefits) are perks or services provided by an employer that have a value, such as:

- Personal use of a company car

- Group-term life insurance over a certain amount

- Employer-paid gym memberships

- Home Purchase Assistance

Valuation

The value of the benefit is “imputed” (estimated) and added to the employee’s gross income for tax purposes. The IRS or local tax authority provides rules for how to calculate the fair market

value of these benefits.

Tax Implications

Even though the employee doesn’t receive cash:

- The value of the benefit is added to their wages (on Form W-2).

- The employee pays income tax, Social Security, and Medicare on the imputed amount.

- The employer also pays payroll taxes on it.

Example 1

Let’s say your employer provides you with:

- Home purchase assistance is valued at $5,000/year.

- Group-term life insurance coverage of $150,000 (only the first $50,000 is tax-free). The imputed income might look like this:

- $5,000 for home purchase assistance

- $120 for the excess life insurance (based on IRS tables)

So, $5,120 would be added to your taxable income, even though you didn’t receive that amount in cash.

Here’s how taxable income works:

Increases Your Taxable Income

Even though you don’t receive cash, the value of the imputed benefit is added to your gross income. This means:

- Your W-2 Box 1 (Wages, tips, other compensation) will be higher.

- You’ll pay federal income tax, Social Security, and Medicare taxes on that higher amount.

Shows Up on Your Pay Stub and W-2

On your pay stub, you might see a line like “Imputed Group Life” or “Imputed HC-EHPAP.” The amount will be added to the gross pay on your pay stub; this does not increase or decrease your take-home pay.

On your W-2, the imputed income is included in:

- Box 1 (Taxable wages)

- Box 3 & 5 (Social Security and Medicare wages), depending on the benefit

- Sometimes Box 12 with a code (e.g., Code C for group-term life insurance)

You Pay More in Taxes

Because your taxable income is higher:

- You may move into a higher tax bracket (if the imputed income is large enough).

- You’ll owe more in taxes unless your withholdings are adjusted to account for it.

Example 2

Let’s say:

- Your salary is $80,000

- You receive $2,000 in imputed income (e.g., employee home purchase assistance)

Your taxable income then becomes $82,000, and you’ll pay taxes on that full amount.

Tax Impact

You’ll pay income tax, Social Security, and Medicare on the total imputed amount.

Your take-home pay doesn’t change, but your tax liability increases.

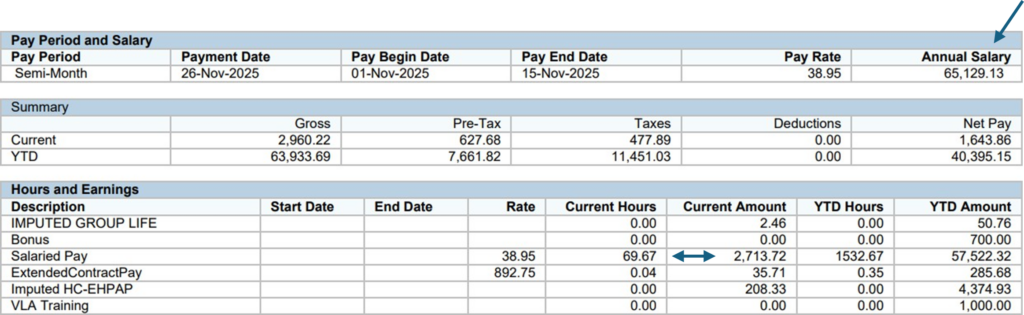

Here’s your pay stub breakdown over 24 pay periods for an annual salary of $65,129.13. Each pay period reflects gross pay of $2,713.72.

Gross pay:

Imputed Group Life:

Extended Contract Pay:

Imputed HC-EHPAP

Current Gross on Pay stub:

$2,713.72

$2.46

$35.71

$208.33*

$2,960.22

*(This amount ($5,000/24 pays) is added to gross pay to calculate taxes properly on Form W-2. It does not increase or decrease your take-home pay).

Your take-home pay can be calculated by using your actual gross pay (less taxes, deductions and pre-tax deductions).

Gross pay:

Less Pre-Tax:

Less Taxes:

Net Pay:

$2,713.71 + Extended Contract Pay $35.71

$627.68

$477.89

$1,643.86 (Actual Take Home Pay)